A Warsh-Led Fed

Regarding rates, the balance sheet, and regime change.

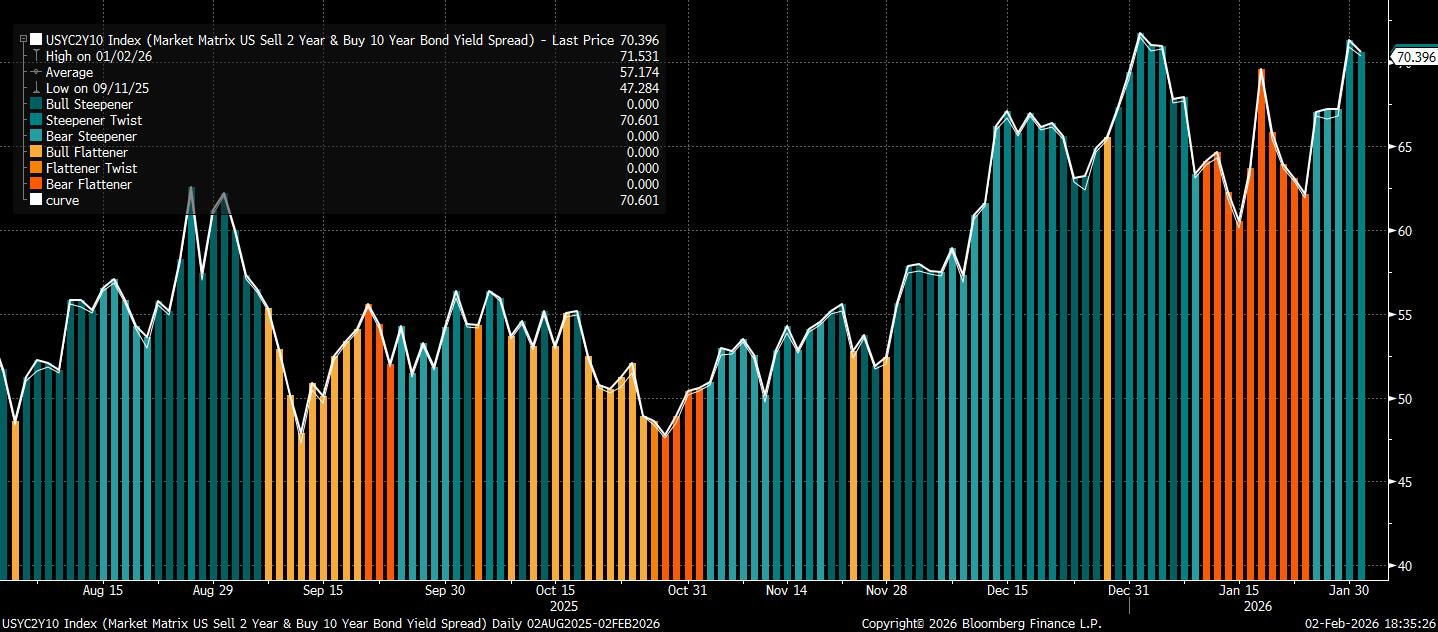

The market had a simple story ready for Kevin Warsh. A hawkish chair, a steeper curve, and a Federal Reserve slowly backing away from the habits of the QE era. Monday disagreed. 2-year yields rose faster than 10s, June cut bets slid toward July, and the first move after the nomination was a modest flattening rather than the steepener investors expected, though the curve still sits towards its steepest level since 2022.

The cross-asset reaction was telling, and maybe captures the uncertainty Warsh brings. Long yields and the dollar firmed, gold and silver softened (albeit for several reasons), and the familiar steepener trade felt premature. Amid all the uncertainty, Warsh’s résumé is solid. Crisis scars from the Fed, market seasoning from Morgan Stanley and Druckenmiller (much like Bessent), and a gift for language that makes him an unusual figure in a profession allergic to plain speech.

The real question is whether Warsh is arriving to tweak the dial on rates or to redraw the borders of what a central bank is meant to do.

Regarding rates… Many commentators call Warsh a hawk, yet the case rests largely on a decade-old event. His 2006–2011 tenure leaned toward higher rates, but his recent statements point the other way. Over recent months, he has favoured easing the benchmark, arguing that stronger growth, powered by AI productivity, need not be inflationary.

In an opinion piece for the Wall Street Journal in November, he had this to say:

“Wall Street and Silicon Valley are booming, and US workers are finally getting a step-up in their real take-home pay. Even so, the benefits of the American juggernaut are yet to be realized fully. Among the chief obstacles is the Fed.”

That optimism deserves a few caveats. The productivity dividend from AI may arrive later and in smaller doses than its champions expect. And even if it does land, history suggests it could lift, not lower, the neutral rate. The late-1990s internet boom delivered real efficiency gains, yet the economy ran hotter, and policy rates settled higher than before.

Regarding the balance sheet… Warsh has been a persistent critic of the Fed’s bond-buying campaigns launched after 2008 and revived during the pandemic. In their place, he has called for a clearer understanding between the Treasury and the central bank about the purpose and limits of asset purchases and sales. The Fed’s “bloated balance sheet,” he argued (again in the November WSJ opinion article), was built to rescue the largest firms in a crisis now past, and could be pared back, with the savings returned to the economy through lower interest rates for households and smaller businesses.

It isn’t obvious that a slimmer balance sheet would do much to tame prices. The Fed’s post-2008 asset surge failed to ignite inflation, and the mirror image, shrinking it, may prove just as blunt an instrument.

Regarding regime change… Warsh’s challenge goes beyond the size of the balance sheet to the way the Fed thinks about inflation itself. He has repeatedly argued that the models guiding policy are aimed at the wrong culprit. In his view, the orthodox focus on consumer demand and wage pressures misses the real driver: the combination of government spending and the money creation that accommodates it.

Speaking with Barron’s in October, Warsh said:

“We need to fundamentally rethink macro, which is a fundamental rethink of the core economic models that the Fed is using—rethink what is the core theory of inflation that the Fed is using, which I think is mistaken.”

The prevailing framework assumes prices rise because households earn and spend too much. He fundamentally disagrees. Inflation, in his telling, is born when the state spends too freely and the central bank prints to keep pace.

It is a distinctly monetarist turn from a former central banker, and a sharp break with the post-crisis consensus that treated inflation as a problem of slack and expectations rather than fiscal arithmetic. If Warsh means what he says, the implication is a Fed more willing to lean against Washington’s ledger.

Warsh would do well to remember the oldest rule in central banking: under-promise and over-deliver. The changes he sketches will require patience, coalition-building and more than a little luck. They may not even be worth the disruption needed to achieve them.

The appointment also settles a different argument. It is an admission that the White House cannot simply bend the Fed to its will. The chair holds one vote of twelve, the window to remake the regional banks has closed, and the courts loom over any future attempt at a purge. After months of noise about firing Jerome Powell, the choice of Warsh signals that the bare-knuckle fight over independence is over.

A former Fed governor with Wall Street credibility and a willingness to challenge orthodoxy was always the natural bridge between change and continuity, and much fits the approach of the current administration.

Whether that detour proves costly will depend on what Warsh actually does once he has the gavel. Markets can live with a hawk or a dove. What they struggle with is a regime in search of itself.

Time for my coffee,

J

Excellent piece on the Warsh appointment. The monetarist turn is what really stands out here, especially the shift from demand-side inflation models to fiscal arithmetic. I've been tracking central bank rhetoric for years and this kind of explicit challenge to the Phillips curve framework feels different. The real test will be whether he can actually lean agaisnt Treasury spending without triggering a political firestorm tho.